Yes, many Veterans who have already used the VA loan program in the past may believe that they are not eligible for another loan through this program. However, it is important to note that this common misconception is simply not true. In fact, Veterans are not limited to just one use of the VA loan program and there are a variety of different scenarios in which you may still be eligible for another VA loan.

Some common eligibility scenarios we encounter include situations where a Veteran sold their previous property and wishes to use their eligibility for a new home, or converting a property to a rental that has a outstanding VA loan. We understand that each Veteran’s situation is unique, and we are here to assist you in finding the best fit for your needs.

It is essential to comprehend the VA’s extensive role in the loan program and the decision-making process for multiple VA loans. The primary function of the VA is to provide an insurance policy that safeguards private lenders in the event of a loan default. The mortgage insurance, commonly known as PMI or MI in the mortgage industry, ensures the protection of the lender’s investment. Notably, this coverage typically amounts to 25% of the loan balance on most VA loans. Consequently, it has significant impacts on various entitlement calculations that may need to be considered.

If a Veteran has previously obtained a VA loan and has successfully sold the property, the Veteran is eligible to have their entitlement fully reinstated. It is important to note that eligibility can be restored multiple times without any negative impact on the Veteran’s entitlement. The only notable implication is the VA funding fee for loans with less than 5% down for subsequent use have an increase to 3.3%.

Also, if the Veteran doesn’t have any outstanding VA loan they have what is called full entitlement, and in this situation there isn’t a maximum loan amount the VA won’t guarantee.

When a Veteran has an existing VA home loan and wishes to purchase another property without settling the existing loan, it leads to a scenario of partial entitlement for the Veteran . In such cases, the VA has a specific price range that it guarantees, and if the sale price falls outside these limits, then the veteran may require to make a down payment or may not be eligible for the program. Therefore, let us proceed to explore the process of partial entitlement calculation.

In order to fully comprehend the intricacies of VA entitlement, it is essential to be aware of the two tiers involved. The first comprises the basic entitlement tier which ranges from $0 to $144,000. The second, also known as bonus entitlement, is applicable for amounts exceeding $144,001 up to the county limit. Fannie Mae and Freddie Mac determine these county limits and they are generally reviewed annually. It should be noted that partial entitlement impacts both tiers and this consideration is significant in fully comprehending the entitlement process.

In order to proceed with your application, it is important that you have a current copy of your Certificate of Eligibility. This document is essential as it provides information on the status of your eligibility tied up on an outstanding VA loan.

To begin, we will utilize the county loan limit and calculate 25% of the limit to establish the maximum entitlement the VA can insure through partial entitlement. From there, we will subtract the amount tied up from the existing VA loan off the Certificate of Eligibility to ascertain the maximum amount remaining eligible. Lastly, we will take that number and multiply it by 4 to determine the maximum loan amount. This will enable us to formulate precise loan ranges based on the VA tiers mentioned earlier.

Tier 1 basic entitlement- Purchase price less than $144,000

If the entitlement charge on the Certificate of Eligibility exceeds $36,000, the veteran cannot obtain a VA loan between $0 – $144,000, but may have a significant amount of tier 2 entitlement. On the other hand, if the entitlement charge is less than $36,000, one should subtract this figure from $36,000 and multiply the result by 4. This calculation would give the maximum loan amount that the VA will guarantee. Should the purchase price exceed this maximum amount, the Veteran will need to make a down payment of 25% of the difference between the sale price and the maximum VA guarantee amount.

Tier 2 bonus entitlement- Purchase price more than $144,001

According to the calculations for the maximum VA guarantee mentioned earlier, we can determine the eligibility range for financing 100% of the purchase price, just like any other VA loan. It is important to note, however, that if the purchase price exceeds the final amount that the VA guarantees, the Veteran may need to make a down payment of 25% of the difference between the sale price and the maximum VA guarantee amount.

Have we confused you yet? Rest assured, we have a multitude of valuable resources at your disposal, including our comprehensive VA entitlement calculator and several detailed examples to reference. Alternatively, you can benefit from speaking directly with one of our knowledgeable VA experts and receive tailored advice on how to maximize your benefits and navigate the process smoothly. Our team is dedicated to ensuring that you fully understand your VA entitlements and can take full advantage of them. Don’t hesitate to contact us today for assistance.

When it comes to defaulting on a VA loan by a Veteran due to reasons such as foreclosure, deed in lieu, or short sale, it is important to understand the potential impact on their eligibility for future VA loans. Typically, when a default occurs, the mortgage servicer will file a claim and this can have a lasting effect on the Veteran’s eligibility. It is important to remember that the VA’s primary role in the mortgage program is that of an insurance provider, as they guarantee 25% of the loan balance at the time of closing.

The good news is with the annual increase in the maximum loan amounts from Fannie Mae and Freddie Mac over the years, we see a steady increase in VA eligibility. The process for remaining entitlement is the same as the calculation described above.

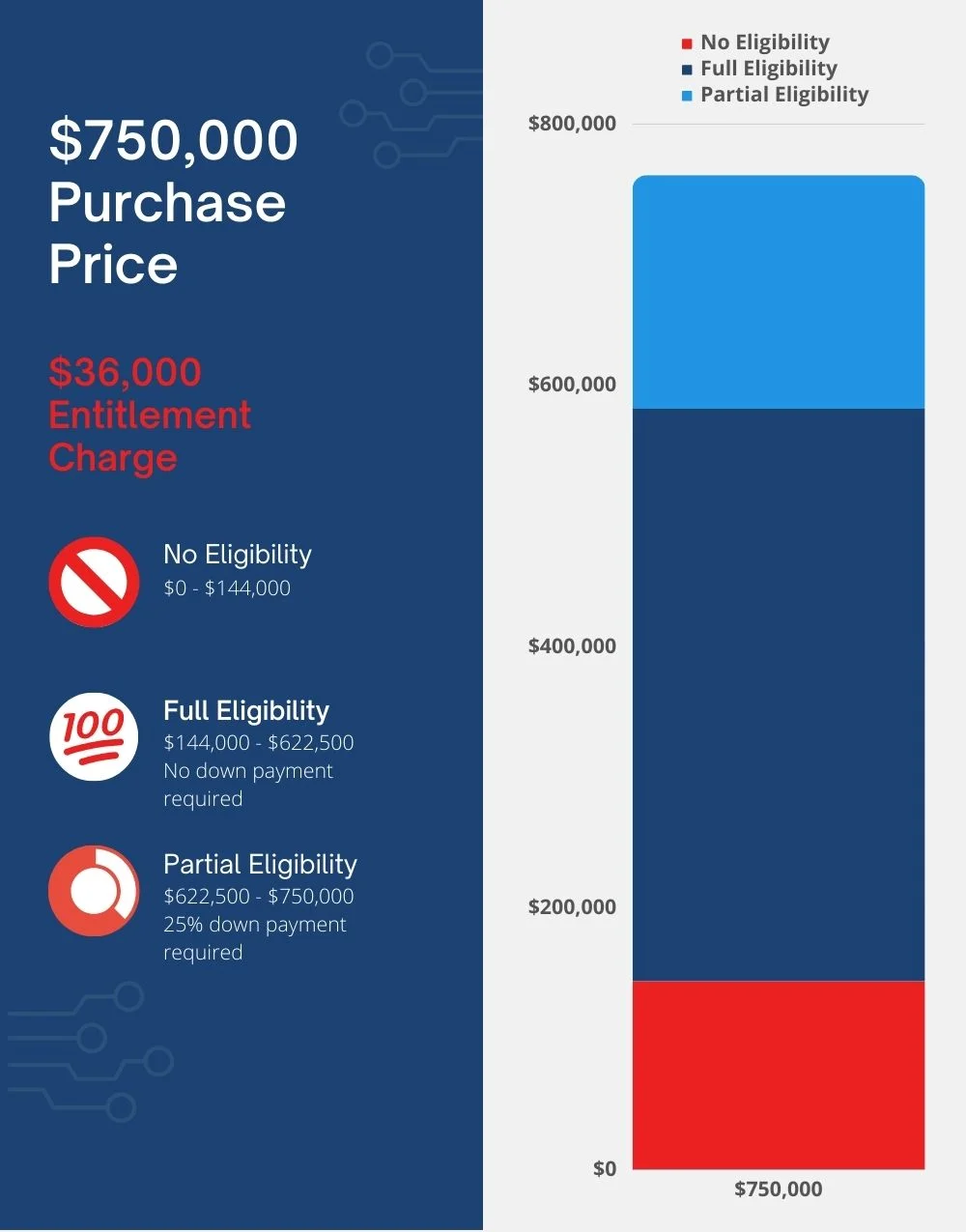

Purchase price $750,000

County Limit $726,200

Entitlement Charge $36,000

First Tier Entitlement

Second Tier Entitlement

Maximum VA Loan without a down payment of $622,550

Minimum down payment $41,950

Final Loan amount $708,050

Purchase price $500,000

County Limit $726,200

Entitlement Charge $12,000

First Tier Entitlement

Full entitlement $0 – $96,000

Partial entitlement $96,001 – $144,000

Second Tier Entitlement

Maximum VA Loan without a down payment of $678,200

Minimum down payment $0

Final Loan amount $500,000

When it comes to defaulting on a VA loan by a Veteran due to reasons such as foreclosure, deed in lieu, or short sale, it is important to understand the potential impact on their eligibility for future VA loans. Typically, when a default occurs, the mortgage servicer will file a claim and this can have a lasting effect on the Veteran’s eligibility. It is important to remember that the VA’s primary role in the mortgage program is that of an insurance provider, as they guarantee 25% of the loan balance at the time of closing.

The good news is with the annual increase in the maximum loan amounts from Fannie Mae and Freddie Mac over the years, we see a steady increase in VA eligibility. The process for remaining entitlement is the same as the calculation described above.

Check if you qualify to buy a home or get a free quote for refinancing within minutes.