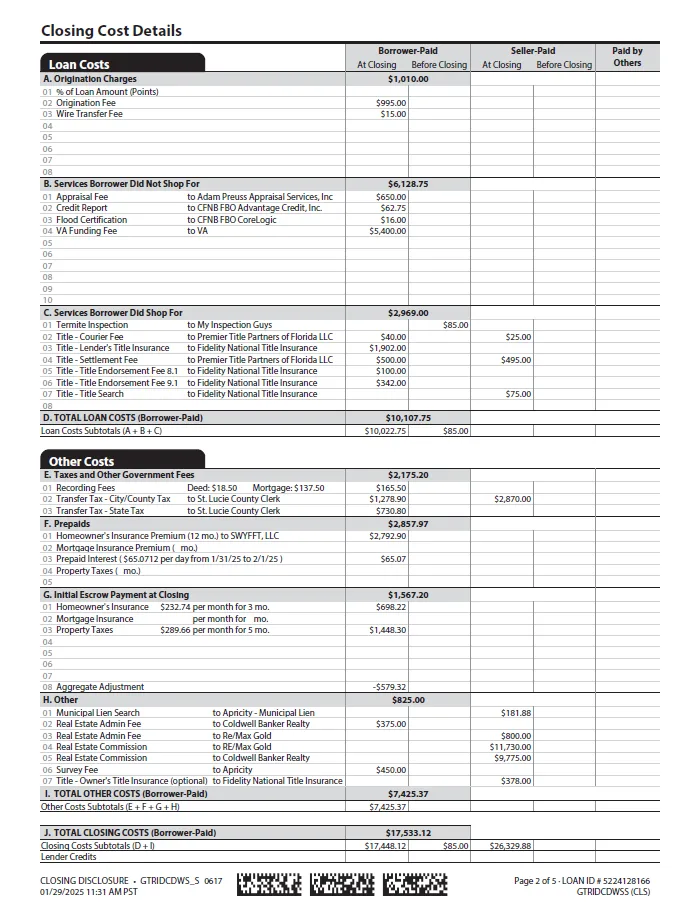

The form is utilized to itemize and detail the closing costs associated with a mortgage transaction, which takes place between the buyer and the seller of the home.

What are some of the common closing costs that you might expect on a typical VA transaction? These expenses can include various fees and charges essential for the smooth completion of the home loan process.

Information and comprehensive options available for paying the closing costs associated with purchasing a home using a VA loan.

For this discussion, we’ll be primarily focused on sections A through L of the closing disclosure document. This document plays a critical role in providing transparency in real estate transactions, enabling both parties to clearly understand the costs involved. Throughout this conversation, we’re going to comprehensively break this important form down section by section, providing detailed explanations and examples of some of the typical charges and fees you might encounter at the closing stage of a real estate transaction. Our goal is to ensure that you have a thorough understanding of each part of the disclosure and what it means for you as a buyer or seller.

These are fees charged by individual lenders. They vary from lender to lender and are charged to cover the cost of processing the transaction. This fee is restricted by the VA at no more than 1% of the total loan amount.

These are prepaid interest fees that the buyer may pay to lower their final interest rate at closing. They are often called points, where one point equals 1% of the final loan amount. These fees are usually optional and vary based on market conditions and the loan amount. We strongly recommend speaking with your loan officer to see if paying these fees is a good value based on the cost and the payment savings over time.

This certification confirms whether a property is in a flood zone that requires flood insurance. If so, federal law requires an additional flood insurance policy.

This fee covers sending funds through the US Federal Reserve system.

These fees are charged to verify employment through electronic verification companies such as The Work Number™.

The VA funding fee is a one-time payment required for most VA home loans. It is designed to offset the costs of the VA loan program, ensuring it remains sustainable for future veterans. The fee is paid directly to the Department of Veterans Affairs (VA) and is a safeguard for mortgage lenders, covering potential losses in case of loan default. The fee amount varies based on the loan type, the borrower’s military service status, the down payment size (if any), and whether the borrower has used the VA loan benefit before. Borrowers can pay the fee upfront or roll it into their loan balance. Certain veterans, like those with service-related disabilities, may be exempt from paying this fee.

The VA appraisal is a requirement on each VA home purchase transaction to determine the value of the property and ensure it meets the VA’s minimum property requirements (MRPs). The cost of the VA appraisal varies based on the location of the property and the type of property being appraised. The cost of these appraisals is regulated by the VA and updated periodically.

The VA appraiser completes Final Inspections to certify any MPR has been completed.

VA requires this inspection on most purchase and cashout refinance transactions unless the property is in an area with low termite infestation. If the inspection indicates an active infestation or any structural damage is present, treatment or repairs will be required.

VA requires a well water test for contaminants anytime there’s an individual drinking water supply.

The VA typically doesn’t require septic inspections on purchase transactions outside of Alaska and certain areas in Idaho, Massachusetts, and Texas. However, it’s worth mentioning that the VA has requirements for Cesspools in the state of Hawaii.

The title company’s primary function is to provide a comprehensive policy designed to protect both the buyer and the lender if there are any liens or claims against the property that may arise upon the transfer of ownership. This is an essential safeguard in real estate transactions, as it ensures that the new owner and the financial institution are protected against potential legal disputes or financial losses. This type of insurance policy is issued in two forms: an owner’s policy, which protects the buyer, and a lender’s policy, which safeguards the lender’s interest. These policies work together to create a secure and trustworthy environment for all parties involved in the property transaction.

Title endorsements are additional insurance coverage attached to a title insurance policy, either for the lender or the homeowner, that protect against specific risks not covered by the standard title insurance policy. Lenders often require them as part of the closing process, and buyers can also request them to protect their interests.

ALTA Endorsements (American Land Title Association)

These are standard endorsements commonly used in the U.S., tailored for lenders or owners:

Gap Endorsement: This endorsement protects the lender or owner against title defects that occur between the time of the title search and the recording of the deed or mortgage.

Access Endorsement: Verifies that the property has legal access to a public road or street.

Tax Endorsement: Covers unpaid or back taxes that could become a lien on the property.

Survey Endorsement: Protects against discrepancies in the survey or boundary lines of the property.

A Closing Protection Letter (CPL) is a document issued by a title insurance underwriter that provides protection to lenders and, in some cases, buyers and sellers against losses caused by the closing agent’s fraud, negligence, or failure to comply with written closing instructions.

If the title company closes the transaction with the buyer and seller, it will typically charge some type of settlement or closing fee.

Often, numerous itemized title fees are charged at closing. Some of these may include document preparation, mailing, wire fees, recording fees, courier fees, and

These are usually associated with remote or out of state closings.

Surveys are typically not required as long as a survey endorsement can be issued from the title company. This depends on the state and sometimes if there’s an existing survey the owners can provide. If not, a new survey will be required.

These are to cover the local recording charges for the deed and mortgage.

These are charged in areas that are subject to state and local taxes and are most common in the Northeastern states. Sometimes these taxes are also charged on refinance transactions.

Depending on your area, county, city, or school, taxes are due annually, semi-annually, or quarterly. To pay these future taxes on time, several months of taxes must be prepaid into an escrow account at closing. On purchase transactions, the seller will issue or collect a tax proration or credit. So, if the taxes are paid in arrears, the seller is issued a credit to the veteran buyer at closing. For those areas where the taxes are prepaid or, in the future, common in the northeastern states, the veteran buyer will need to pay the seller back for those taxes.

Note that some states have real estate tax exemptions for disabled veterans.

When insurance is escrowed it’s paid a year in advance at closing on a home purchase. For refinancing enough funds are collected to pay the annual premium based on the month of renewal.

When a mortgage is closed typically the first mortgage payment is typically due the 1st day of the 2nd month preceding the closing date. For example, closing on January 15 the first payment due date is usually March 1st. Mortgage payments made are for the interest for the previous month. So our March mortgage payment is collecting for the month of Februarys’ interest. The unpaid interest from our closing date on January 15 to February 1 is therefore collected and paid at the time of closing.

.

The veteran can pay their own closing costs at the settlement. Paying your own closing costs out of pocket can potentially provide a benefit in a tight housing market where the sellers are considering multiple offers. If the seller is considering offers with similar offer prices but some are asking for them to pay the buyers’ closing cost and other are not, they may favor the offers where they don’t have to pay any cost to maximize their potential profit.

Seller concession is the most popular and widely used tool to reduce or eliminate closing costs. When the purchase offer is being made to the seller, it can be stated that a portion of the final sale price may go toward the veteran’s closing costs. These concessions can go toward the following costs:

Note that VA restricts no more than 4% of the final sale price to go toward prepaid, excessive discount points, and the paydown of credit balances or judgements. Normal closing costs and discount points would not be considered part of the 4% threshold.

The VA permits gift proceeds to be used for closing costs and or downpayments with proper documentation. These gifts may come from various donors such as family or friends.

The lender can also issue credit to go towards closing cost. Typically, this is partly due to the veteran who opt to choose an higher interest rate in order to generate these credits, so there’s a tradeoff that need to be considered.

There are a few national veteran specific programs that connect veterans with local real estate agents. We have partnered with the Veterans Real Estate Benefits (VREB ) Program and Agent Network to provide nationwide Veteran -Certified Agent coverage and Industry Leading Membership Reward Benefits (or Realtor Closing Cost Credit). In addition, they provide access to top Veteran homeowner insurance companies as well as Homebuyer education and real estate services, all free of charge. Certain restrictions apply. Contact us today for more information. VREB program is not owned or operated by Community First National Bank, and use of the program is voluntary and not a qualifying condition of your loan

There are several national, state, and local programs that may be able to help with closing costs assistance. This can come from bond or grant programs that may come with eligibility restrictions and homebuyer education requirements. As a national bank in Kansas, we have access to the federal loan bank of Topeka grant and bond programs in Kansas, Oklahoma, Colorado, and Nebraska. It’s advised to do your homework with any of these programs.

SmartVALoans.com is a service of Community First National Bank

VA Approved Lender, not a government agency.

Member FDIC Insured #35585 – Equal Housing Lender

NMLS ID #449196 NMLS Consumer Access Page

Community First National Bank

11900 W. 87th Street Pkwy, Suite 115

Lenexa KS 66215